U.S. Expats: 2026 RMD Guide

2026 RMD Roadmap for US Expats

Navigating Required Minimum Distributions (RMDs) while living abroad adds a layer of multi-jurisdictional complexity that standard retirement software simply isn't built to handle. When US tax code requirements intersect with local European tax treaties, a single misstep can trigger dual-taxation or steep compliance penalties.

This guide breaks down the core 2026 US frameworks and maps them directly to the local tax treatments across major European expat hubs.

1. 2026 US RMD Core Framework

Before factoring in local European legislation, your distributions must satisfy the baseline IRS rules for the 2026 tax year:

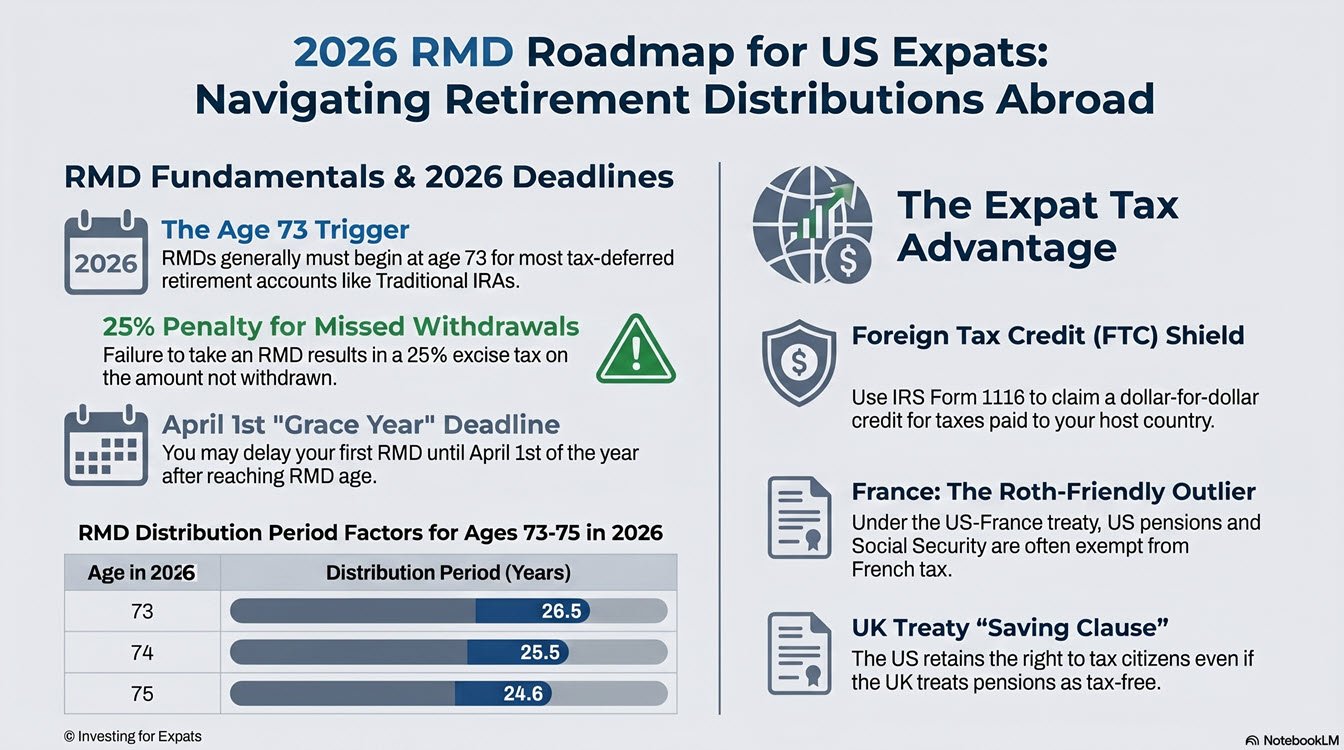

The Age Threshold: Under the SECURE 2.0 Act framework, the RMD mandatory start age remains firm at 73. If you turn 73 during 2026, you are officially required to take a distribution for this tax year.

Deadlines & Stacking Risks: Your very first RMD can be delayed until April 1, 2027. However, delaying means you must take your second RMD by December 31, 2027. Stacking two distributions into one calendar year can create a major income spike, potentially exposing your income to the top 37% ordinary US marginal tax bracket or pushing you into higher host-country progressive brackets.

The Penalty Matrix: Failing to distribute the correct amount by the deadline carries a 25% excise tax on the unwithdrawn amount. This penalty drops to 10% if the error is proactively identified and corrected within a standard two-year correction window.

Aggregation Boundaries: Traditional, Rollover, SEP, and SIMPLE IRAs can be aggregated—meaning you calculate the RMD for each but can pull the total from a single account. Workplace qualified plans like 401(k) and 403(b) accounts cannot be aggregated with IRAs; each plan must satisfy its own independent RMD.

The Roth Exemption: RMD rules do not apply to your own Roth IRAs or designated Roth workplace accounts during your lifetime. Growth continues tax-free on the US side.

2. Interactive 2026 RMD Estimator

To quickly establish baseline distribution requirements using the current IRS Uniform Lifetime Table (Table III), utilize the calculator below to model your distribution factor and estimated structural obligations.

3. European Host Country Treatment Matrix

While the IRS mandates that you must take the money out, your country of residence determines how that distribution is penalized, protected, or paired with foreign tax mechanisms.

2026 RMD Reference Guide for US expats in Europe

4. Critical Expat Pitfalls to Monitor

The FEIE Exclusion Illusion: A common misconception among expats is that the Foreign Earned Income Exclusion (Form 2555) can shield retirement distributions. It cannot. The FEIE applies strictly to active, earned compensation (salaries, wages, self-employment income). RMDs are categorized entirely as unearned passive income.

Currency Conversion Divergence: Your RMD is calculated strictly on the USD valuation of your accounts as of December 31, 2025. However, the host country will assess the tax based on the spot exchange rate at the exact moment the distribution lands in 2026. Dramatic shifts in the EUR/USD or GBP/USD cross-rates can create artificial currency gains or sudden shortfalls in expected local purchasing power.

The Local Health Charge Surcharge: In nations like France, while the income tax treaty protects the RMD from standard income tax via credits, social assessments (prélèvements sociaux) can occasionally sneak onto returns depending on your specific local health system affiliation or ownership of an EU S1 form. Always verify local healthcare integration status prior to executing large withdrawals.

IRS and European reporting requirements for retirement accounts: visit this page to learn the explicit reporting thresholds and rules for FBAR, FATCA, Form 8833, and the inverse requirements imposed by major European host nations.

-

IRA Required Minimum Distribution (RMD) Table for 2026 - SmartAsset.com

2026 RMD Reference Guide - Charles Schwab

Retirement plan and IRA required minimum distributions FAQs | Internal Revenue Service

Retiring Abroad as an American: U.S. Tax Rules, Filing Requirements, and Planning Strategies

US-UK tax treaty guide (2026): Avoid double taxation - Taxes for Expats

Income Tax on US Pensions and Social Security

The US-France Tax Treaty's Hidden Advantage for American Retirees - IMI Daily

What Happens to Your Roth IRA If You Retire to Europe? - Liberty Atlantic Advisors

IRAs for Retirees Living Abroad: Managing Distributions, Taxes, and Strategies

Last updated: May 28, 2026