A Comprehensive Report on U.S. Estate & Inheritance Tax for American Expatriates

U.S. Estate & Inheritance Tax for American Expatriates

For American expatriates, navigating the overlap between U.S. federal tax laws and the succession rules of their host country is a complex but essential task. While you may live thousands of miles from the U.S., your status as a "U.S. person" means the IRS maintains a permanent seat at your estate planning table.

Below is an overview of the landscape for 2026, incorporating the latest legislative updates.

1. The Global Reach of U.S. Estate Tax

The U.S. is one of the few countries that taxes its citizens on their worldwide assets, regardless of where they reside. This means your home in Tuscany, your bank accounts in London, and your brokerage accounts in New York are all part of your "gross estate" for U.S. tax purposes.

Key Thresholds for 2026

Under the One Big Beautiful Bill Act (OBBBA) signed in 2025, the sunset of the 2017 TCJA provisions was averted, and exemptions were expanded:

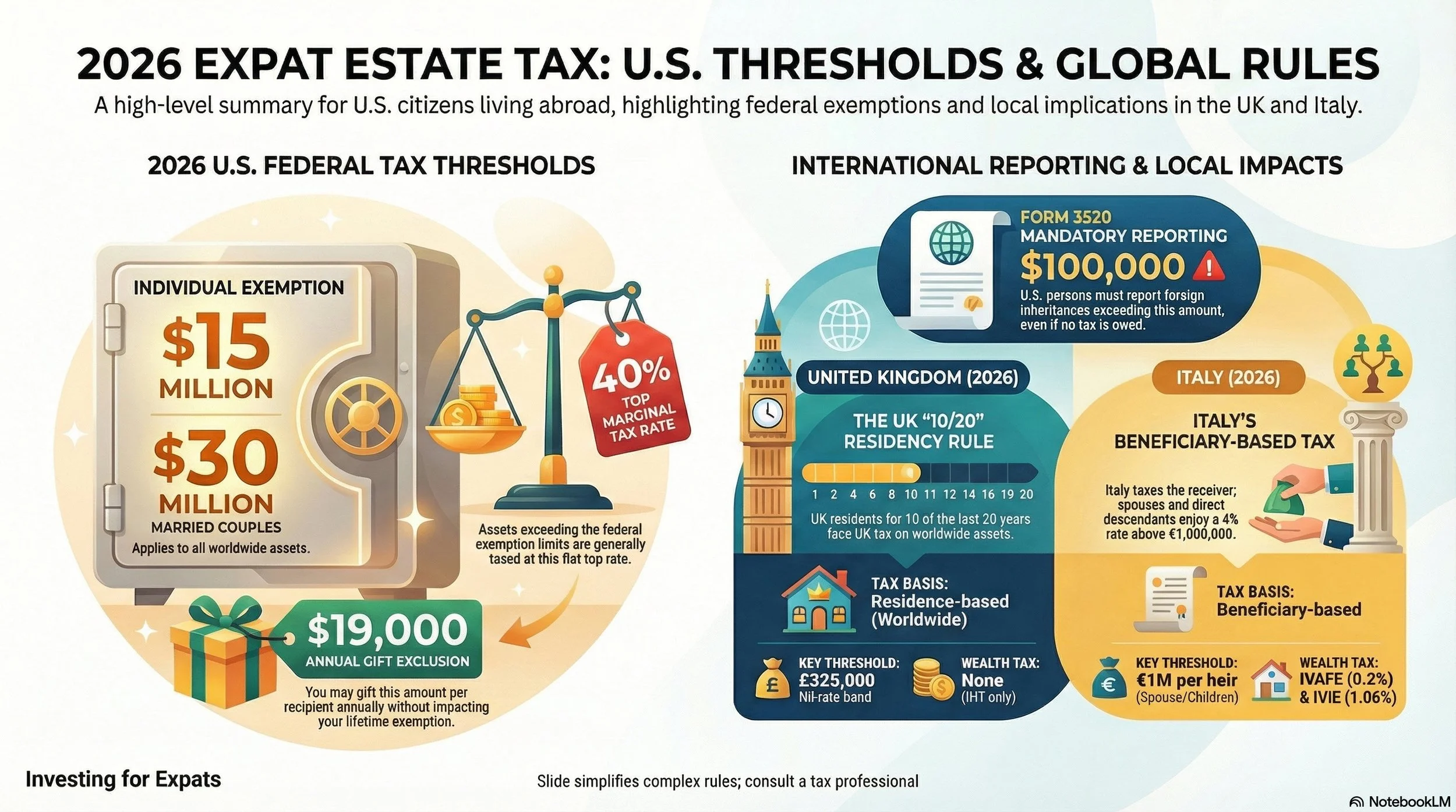

Individual Exemption: $15,000,000 (up from $13.99M in 2025).

Married Couple Exemption: $30,000,000 with proper planning and portability elections.

Tax Rate: Assets exceeding these amounts are generally taxed at a top marginal rate of 40%.

2. Gift Tax & Lifetime Transfers

Giving away assets while you are alive is a common strategy to reduce the size of your taxable estate. However, U.S. expats must be mindful of annual limits:

Annual Exclusion: In 2026, you can gift up to $19,000 per recipient without using any of your lifetime exemption.

Non-U.S. Citizen Spouses: Unlike the "unlimited marital deduction" available for U.S. citizen spouses, gifts to a spouse who is not a U.S. citizen are capped. For 2026, this limit is $194,000.

3. The "Inheritance Tax" Misconception

It is important to distinguish between Estate Tax (taxing the giver's estate) and Inheritance Tax (taxing the receiver).

Federal Level: The U.S. does not have a federal inheritance tax. If you inherit money from a foreign person, you generally owe no U.S. tax on the principal.

Reporting (Form 3520): While the inheritance isn't taxed, you must report it if the value exceeds $100,000 from a foreign individual or estate. Failure to file can result in penalties starting at 5% of the inheritance per month.

4. International Complications

Double Taxation & Treaties

Many European countries (such as the UK, Germany, and France) have their own inheritance or estate taxes. To avoid paying twice, the U.S. maintains Estate Tax Treaties with several nations. These treaties often:

Determine which country has the primary right to tax specific assets (like real estate).

Provide for a Foreign Death Tax Credit, allowing you to offset U.S. tax with taxes paid to your host country.

State-Level Domicile

Even if you live abroad, you may still be considered "domiciled" in a U.S. state for tax purposes. Some states (like Oregon or Washington) have estate tax thresholds as low as $1M–$2M, which are far lower than the federal $15M limit.

5. Checklist for Expats

Review Your Will: Ensure you have a will that is valid in both the U.S. and your country of residence. Some experts recommend "situate wills"—separate documents for assets in different jurisdictions.

Monitor Domicile: If you still vote, hold a driver's license, or own property in a U.S. state, you may be subject to that state's estate tax.

Check PFICs: Inherited foreign mutual funds (PFICs) can trigger punitive "phantom income" taxes and complex reporting requirements (37% top rate plus compounding interest).

UK vs. Italy: US Expat Estate Tax Comparison

Country-Specific Showdowns:

Estate and Inheritance Tax in the UK and Italy

For U.S. citizens living in the UK and Italy, the intersection of local succession laws and U.S. federal tax is governed by two very different frameworks. While the UK has undergone a massive structural shift in its inheritance tax (IHT) regime for 2026, Italy remains one of the more tax-favorable jurisdictions for heirs, provided the 2026 wealth tax updates are managed.

The United Kingdom: The New Residence-Based Frontier

As of April 6, 2025, the UK officially moved away from the "domicile" system to a residence-based regime. This has profound implications for U.S. expats in 2026.

The "10/20" Rule and the IHT Tail

The Threshold: If you have been a UK resident for 10 out of the last 20 tax years, your worldwide assets are now within the scope of UK Inheritance Tax (40% rate above the £325,000 nil-rate band).

The "Tail": Even if you leave the UK, you remain subject to UK IHT for a "tail" period. This ranges from 3 to 10 years depending on how long you lived in the UK.

Treaty Protection: The US-UK Estate Tax Treaty remains a vital shield. It provides "tie-breaker" rules that can often determine you are "treaty domiciled" in the U.S., potentially limiting the UK’s ability to tax your non-UK assets even if you meet the 10-year residency test.

Trust Changes

Historically, "Excluded Property Trusts" protected non-UK assets indefinitely. Under the 2026 rules, this protection is gone for "Long-Term Residents." If the settlor is a long-term resident at the time of a 10-year anniversary charge or death, the trust assets may be hit with UK tax.

Italy: Generous Exemptions and Wealth Tax Realities

Italy is often considered a "tax haven" for inheritance compared to the UK or U.S., but it requires careful reporting of foreign-held assets.

Italian Inheritance Tax Rates (2026)

Italy taxes the beneficiary, not the estate. Rates depend on the relationship to the deceased:

Spouse and Direct Descendants: 4% tax, but only on the amount exceeding €1,000,000 per heir.

Siblings: 6% tax on the amount exceeding €100,000.

Other Relatives (up to 4th degree): 6% tax with no exemption.

Unrelated Parties: 8% tax with no exemption.

The 2026 Wealth Tax (IVAFE & IVIE)

While the inheritance tax is low, Italian residents must pay annual wealth taxes on foreign assets, which can "leak" the value of an estate over time:

IVAFE (Financial Assets): Generally 0.2% of market value (increased to 0.4% in "blacklisted" jurisdictions).

IVIE (Foreign Real Estate):1.06% per year (reduced to 0.4% for a primary residence).

The "Step-Up" Conflict: Unlike the U.S., which grants a "step-up in basis" to fair market value upon death, Italy may not recognize this for capital gains purposes when the heir eventually sells the asset.

QUICK-REFERENCE FACT SHEET:

Estate & Succession Planning for U.S. Expats in the UK vs. Italy (2026)

This fast-sheet provides a streamlined overview of key data points and rules effective as of January 1, 2026, considering the relevant U.S. and local tax legislation.

US Expat Estate Planning: UK vs. Italy

Critical U.S. Reporting Thresholds for 2026

Federal Estate Exemption: $15,000,000 per person.

Form 3520 (Inheritance Report): Required if a U.S. person receives over $100,000 from a non-U.S. person's estate.

FinCEN 114 (FBAR): Required if combined value of foreign financial accounts exceeds $10,000 at any time during the calendar year.

Additional information about the U.S.-Italy Estate and Gift Tax Treaty for U.S. Citizens Domiciled in Italy is available here.

-

Internal Revenue Service (IRS): Estate and Gift Tax Updates for 2026; Form 3520 Instructions.

One Big Beautiful Bill Act (OBBBA) of 2025: Permanent extension of TCJA individual tax provisions.

Morgan Lewis: "IRS Announces Increased Gift and Estate Tax Exemption Amounts for 2026."

Taxes for Expats (TFX): "Foreign inheritance tax: US reporting requirements (2026)."

PwC Worldwide Tax Summaries: "United States - Individual - Foreign tax relief and tax treaties."

UK Gov Guidance (2025/26): "Inheritance Tax if you're a long-term UK resident" (The 10/20 Test).

US-UK Estate & Gift Tax Treaty (1979): Specifically Article 4 (Fiscal Domicile) and Article 9 (Relief from Double Taxation).

Italian Revenue Agency (Agenzia delle Entrate): Circular 139/2024 (Abolition of "succession aggregation" and updated IVAFE/IVIE rates).

Taxes for Expats (TFX): "US-Italy Estate Tax Treaty Guide (Updated 2026)."

Saffery: "Inheritance tax reforms for UK non-doms: The move to residence-based IHT."

Last Updated: Mar. 24, 2026