Efficacy and Tax Consequences of U.S. TOD and POD Accounts for American Expatriates

Summary

This report provides a comprehensive analysis of the legal validity, procedural requirements, and complex tax implications of U.S.-based Transfer on Death (TOD) and Payable on Death (POD) accounts for United States citizens who reside and pass away abroad.

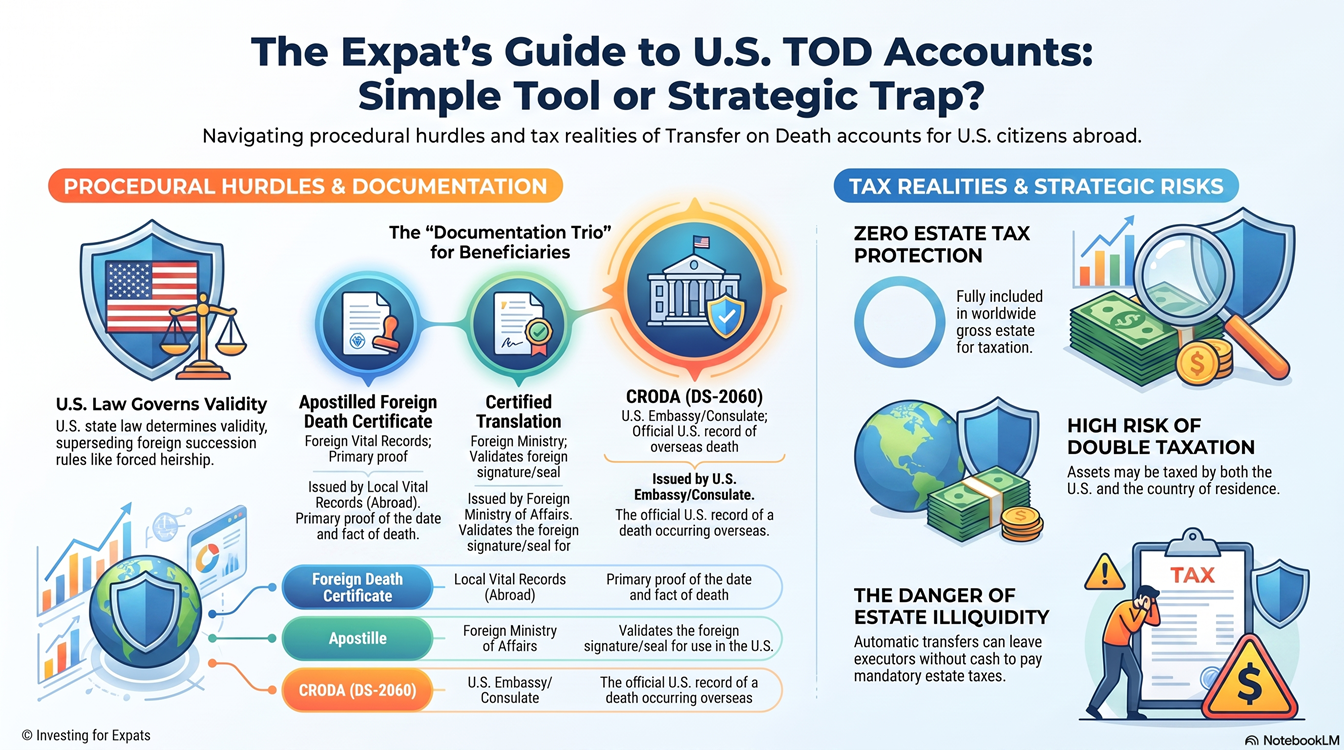

The core finding regarding validity is unequivocal: a properly established TOD or POD designation on a U.S.-based financial account is legally valid and will be honored. The governing authority is the U.S. state law applicable to the financial institution where the account is held, not the laws of the decedent's foreign country of residence. The primary challenge for beneficiaries is not one of legal right but of procedural execution. Claiming the assets requires navigating a specific set of documentation requirements to prove the death to the U.S. financial institution. This process is complicated by the international context, necessitating key documents such as a foreign-issued death certificate authenticated via an Apostille (for Hague Convention countries) and the U.S. Department of State's Consular Report of Death of a U.S. Citizen Abroad (CRODA).

From a tax perspective, the decedent's estate faces a dual exposure. As a U.S. citizen, the decedent's worldwide assets are subject to the U.S. federal estate tax. Concurrently, the country of residence may impose its own inheritance or estate tax on the decedent's assets. It is critical to understand that TOD and POD assets are included in the decedent's gross estate for U.S. tax purposes and offer no protection from estate tax liability.

Mechanisms to mitigate this potential double taxation exist, primarily through a network of bilateral U.S. estate and gift tax treaties, which allocate taxing rights between countries, and the statutory U.S. Foreign Death Tax Credit, which can offset taxes paid to a foreign jurisdiction against U.S. estate tax owed.

Despite their apparent simplicity, this analysis concludes that TOD and POD accounts are often a suboptimal estate planning tool for U.S. expatriates. Their inflexibility can precipitate significant unintended consequences, including estate liquidity crises, the disruption of sophisticated tax-planning strategies, and complications when dealing with minor or special needs beneficiaries. For the majority of U.S. citizens living abroad, a revocable living trust remains a vastly superior vehicle for the comprehensive and tax-efficient management of a cross-border estate.

Strategic Considerations and Recommendations for Expatriates

Evaluating TOD/PODs vs. Revocable Living Trusts

While TOD and POD accounts offer a simple method for non-probate transfers, they are often inferior to a revocable living trust, especially in the context of an international estate.

Flexibility and Control: A trust is a highly flexible instrument. It can be drafted to accommodate complex distribution plans, such as staggering payments to a young beneficiary or holding assets for their lifetime. Crucially, a trust provides a mechanism for managing assets in the event of the owner's incapacity, a situation where a TOD designation is entirely ineffective, as it only triggers upon death.

Comprehensive Asset Management: A trust can serve as a single, centralized vehicle for holding and managing assets located in multiple jurisdictions. This allows for a coordinated and unified estate plan. TODs, by contrast, are piecemeal. They must be established for each individual account, creating a fragmented plan that is prone to errors, omissions, and inconsistencies as life circumstances change.

Tax Planning: Trusts are indispensable tools for sophisticated estate tax planning. They can be structured to create sub-trusts upon death, such as a credit shelter trust (or bypass trust) and a marital trust, which are designed to make maximum use of both spouses' federal estate tax exemptions. A TOD designation, by transferring assets directly to a beneficiary, completely bypasses the trust and can inadvertently nullify this critical tax planning, potentially leading to a significant and unnecessary estate tax liability.

The Pitfall of Estate Illiquidity

One of the most severe and often unforeseen dangers of relying heavily on TOD and POD accounts is the creation of an estate liquidity crisis. Upon death, the most liquid assets—cash in bank accounts and marketable securities in brokerage accounts—are transferred directly and immediately to the named beneficiaries. This can leave the estate's executor with only illiquid assets, such as real estate or interests in a closely held business.

However, the executor remains legally responsible for paying all of the decedent's final debts, administrative expenses (legal and accounting fees), and, most importantly, any U.S. and foreign estate or inheritance taxes that are due. With no cash in the probate estate, the executor is forced to either sell the illiquid assets, perhaps at an inopportune time, or demand that the TOD beneficiaries return a portion of their inheritance to the estate to cover these liabilities. This process of "clawback" is not only administratively burdensome but is also a common source of conflict and litigation among heirs.

Addressing Beneficiary Complexities

TOD accounts are ill-suited for situations involving beneficiaries who are not capable of managing a direct, outright inheritance.

Minors: Naming a minor (typically under 18) as a direct beneficiary of a TOD account is highly problematic. Minors cannot legally own or manage significant assets directly. This would necessitate a court proceeding to appoint a guardian or conservator to manage the funds until the child reaches the age of majority. A simpler, but still imperfect, alternative is to name an adult custodian for the minor under the Uniform Transfers to Minors Act (UTMA). A trust is a far superior vehicle, allowing the creator to specify precisely how and when funds should be used for the child's benefit and at what age they should receive full control.

Special Needs Beneficiaries: For a beneficiary who relies on means-tested government benefits, such as Supplemental Security Income (SSI) or Medicaid, receiving an outright inheritance via a TOD account can be catastrophic. The sudden influx of assets will likely render them ineligible for these essential benefits until the inheritance is spent down. The proper approach is to leave assets for their benefit in a specially drafted Special Needs Trust, which is designed to supplement, not replace, government benefits.

Contingent Beneficiaries: A TOD designation is a simple A-to-B transfer. If the primary beneficiary predeceases the account owner and no contingent (or backup) beneficiary has been named on the account form, the designation fails. The asset then reverts to the decedent's estate and must pass through probate, entirely defeating the primary purpose of the TOD account.

Actionable Recommendations for U.S. Citizens Residing Abroad

Given the complexities of cross-border estates, U.S. expatriates should adopt a comprehensive and strategic approach to their estate planning.

Conduct a Global Asset Inventory: The first step is to create a detailed inventory of all worldwide assets, noting their type, value, location, and how they are titled. This provides a clear picture of the total gross estate for tax purposes.

Seek Dual-Qualified Counsel: It is imperative to engage legal and tax advisors who possess expertise in both U.S. estate planning and the inheritance and tax laws of the country of residence. A plan designed solely from a U.S. perspective is likely to be ineffective or create problems abroad, and vice versa.

Prioritize a Revocable Living Trust: For most expatriates with a multi-jurisdictional estate of significant value, a U.S.-based revocable living trust should be the central organizing document of their estate plan. It provides the necessary coordination, flexibility for complex distributions, planning for incapacity, and the structure required for sophisticated tax mitigation strategies that TOD accounts cannot offer.

Use TODs Strategically, If At All: TOD and POD accounts should not be the foundation of an expatriate's estate plan. They may be used sparingly for specific, limited purposes, such as providing immediate access to a modest amount of cash for a single, responsible adult beneficiary to cover final expenses. A more effective strategy is to name the revocable trust as the beneficiary of TOD and POD accounts. This approach combines the probate-avoidance benefit of the TOD with the centralized control and sophisticated distribution capabilities of the trust.

Regularly Review Beneficiary Designations: An estate plan is not a static document. Significant life events—such as marriage, divorce, the birth of a child, or the death of a beneficiary—necessitate a thorough review of all beneficiary designations on all accounts (TOD, POD, retirement, insurance) to ensure they remain aligned with current wishes and the overarching structure of the comprehensive estate plan.

Additional Information

For a deep dive into this subject, download the full report Efficacy and Tax Consequences of U.S. Transfer on Death (TOD) Accounts for American Expatriates (28 Pages, PDF Format).

You can also chat with our research assistant here.

Lat modified on Jul. 8, 2026