Financial planning and investment strategies for American citizens relocating to Europe

Global Adventures, Secure Finances:

Success Guide for the American expat

For American citizens living and working in Europe, the financial landscape presents unique challenges and opportunities.

This platform serves as a comprehensive resource for both expatriates and the advisors who support them, offering in-depth insights into the complex world of cross-border finance.

Latest Articles and Books:

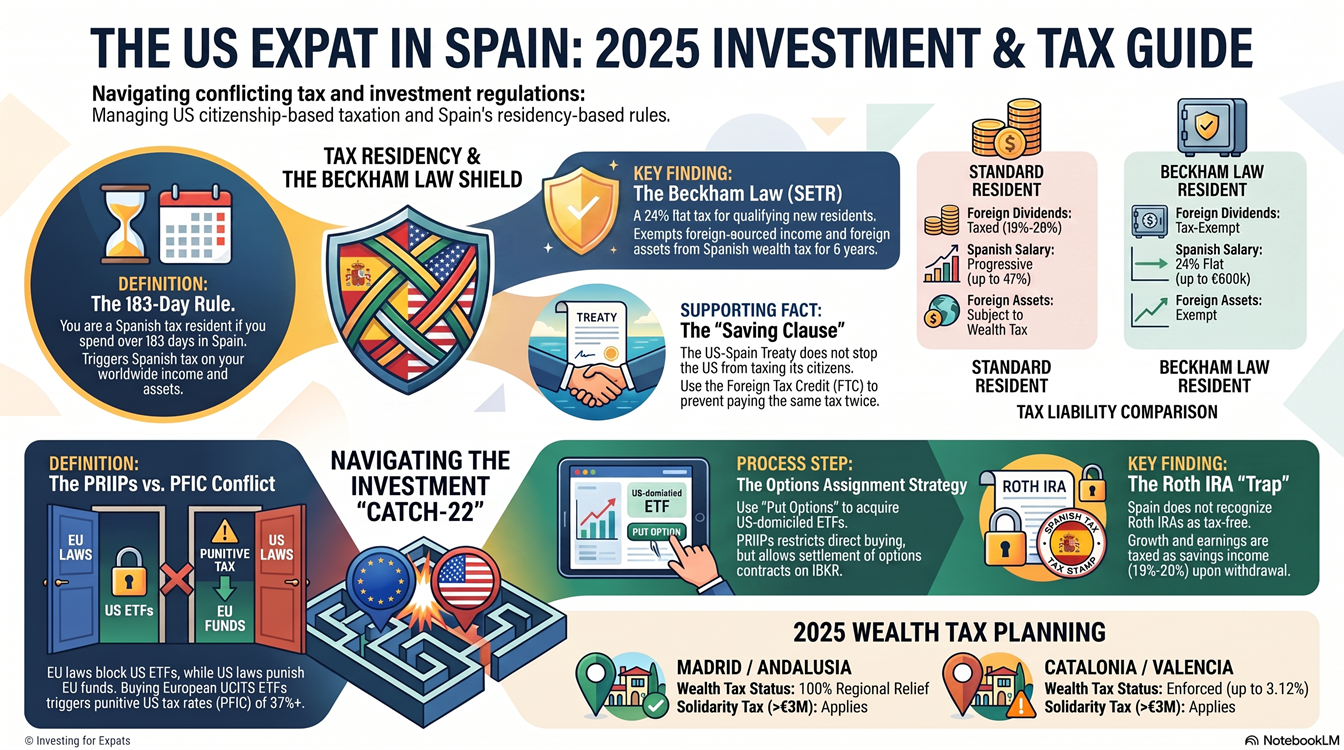

The Beckham Law, officially known as the Special Expats’ Tax Regime (SETR), is considered the most powerful tax planning tool for foreigners moving to Spain, having been recently updated for 2025 under the "Startup Law".

The core mechanism of the Beckham Law is that it allows qualifying individuals to be taxed as non-residents for the year of their arrival plus the five subsequent years, offering a total of six years of significant tax advantages. Read more…

This comprehensive guide outlines the tax and residency landscape for U.S. citizens moving to Portugal in 2026, highlighting a transition toward more specialized and regulated environments. It details the shift from the broad NHR tax status to the activity-focused IFICI regime, which offers a 20% flat tax rate for specific high-value professions. The text warns of complex U.S. federal obligations under the One Big Beautiful Bill Act and the persistent risk of being taxed by California after relocating abroad. Strategic advice is provided on selecting appropriate visas, such as the D7 or Digital Nomad options, while avoiding "tax traps" like Passive Foreign Investment Companies. Read more…

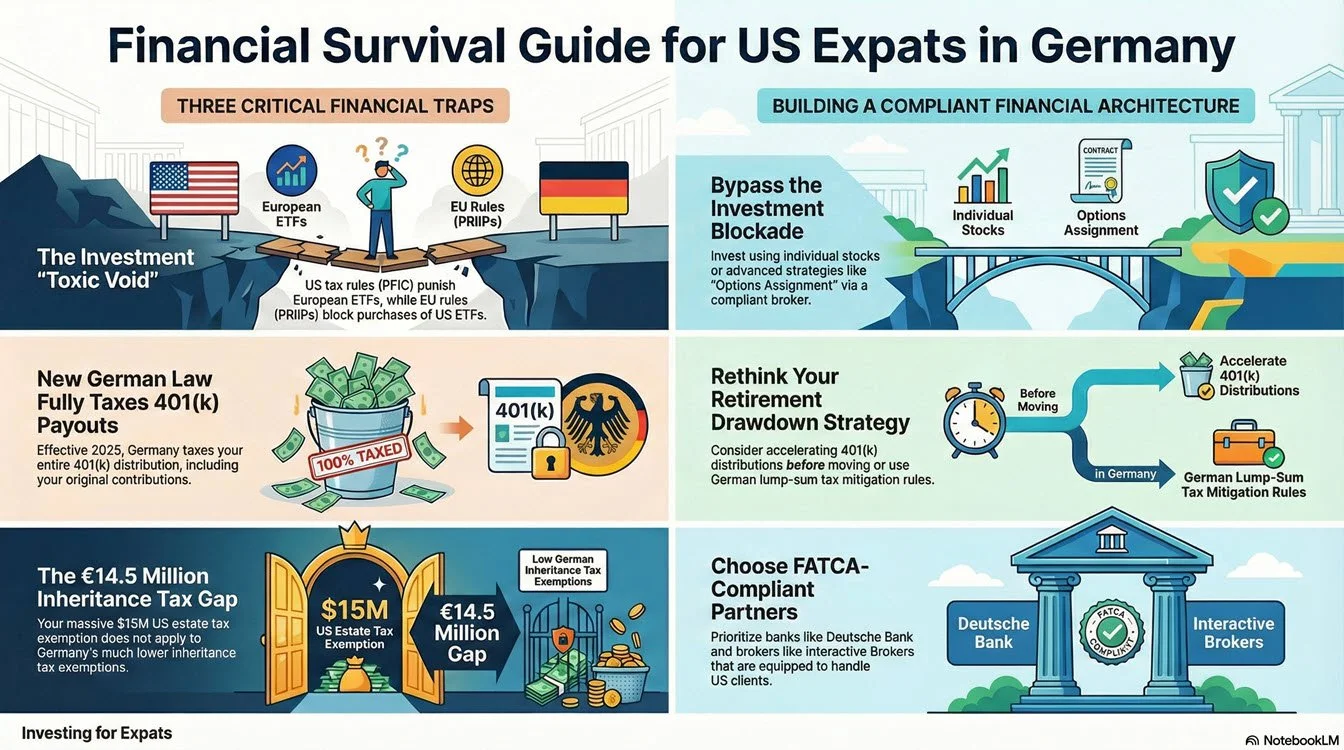

Financial planning for US citizens moving to or living in Germany in 2026

This detailed report, "Investing from Germany: Financial planning and investment strategies for US persons relocating to or residing in Germany in 2026," serves as a vital guideline for navigating one of the most complex and challenging cross-border regulatory environments globally. As the 2026 fiscal landscape evolves with new German laws and revised US inflation parameters, this guide provides the "defensive financial architecture" needed to safeguard and enhance your wealth. Read more…

Last Updated: Jul 7, 2026

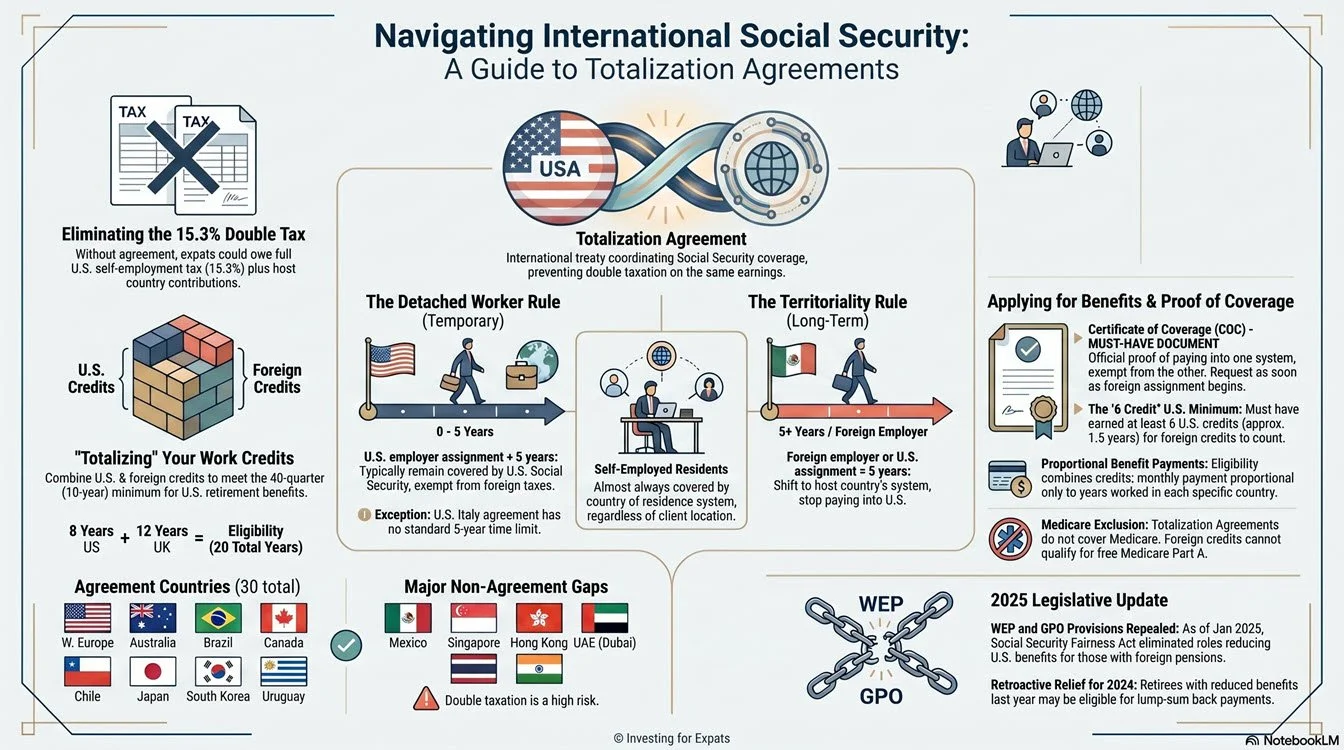

Totalization Agreements are international treaties designed to protect workers from being taxed twice for social security. These agreements primarily benefit expats, detached workers, and self-employed individuals by determining which country’s system covers their earnings, based on factors such as residency and assignment length. Beyond preventing double taxation, these treaties allow individuals to combine work credits from multiple nations to meet the minimum requirements for retirement or disability benefits. While the United States has established such agreements with approximately 30 countries, many popular destinations remain uncovered, potentially leaving workers liable for dual contributions. Read more

Financial planning for US citizens moving to or living in the United Kingdom in 2026

For American citizens residing in the United Kingdom, 2026 represents a fiscal watershed. Two tectonic shifts in tax policy have collided: the United Kingdom’s historic abolition of the 200-year-old "non-dom" remittance basis, and the United States’ enactment of the "One Big Beautiful Bill Act" (OBBBA), which permanently codifies the Tax Cuts and Jobs Act era.

The era of "benign neglect"—where one could rely on the remittance basis to shield foreign wealth while ignoring US tax nuances—is over. In this new landscape, passivity is not just inefficient; it is punitive. Read more…

Investing Abroad for U.S. Citizens and Resident Aliens

Investing while living abroad as a U.S. citizen or resident alien presents a unique and often bewildering set of challenges. Beyond the universal goals of wealth creation and financial security, U.S. expatriates must navigate a complex web of U.S. tax laws, foreign regulations, and cross-border financial intricacies.

Failure to understand and address these complexities can lead to significant financial penalties, missed investment opportunities, and considerable stress. This article delves into the key issues every U.S. person investing overseas needs to consider. Read more …

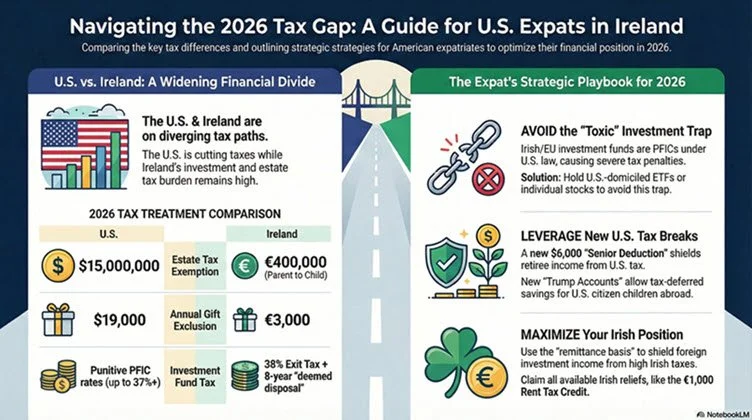

Ireland: Financial Planning and Investing Strategies for U.S. Citizens

Are you a U.S. citizen living in Ireland? If you are still using tax strategies from 2024 or 2025, you are likely leaving money on the table—or walking into a compliance minefield.

The fiscal landscape has shifted tectonically. The collision of the United States' new One Big Beautiful Bill Act (OBBBA) and Ireland’s Budget 2026 has created a confusing new reality of conflicting tax rates, novel deductions, and dangerous investment traps. Read more…