IRS and European Reporting Requirements for Retirement Accounts

FBAR vs. FATCA Reporting Guide (2026)

Operating as a US expat in Europe means you don't just report what you earn—you must meticulously report what you own. When it comes to retirement accounts, the IRS, FinCEN, and European tax authorities use overlapping frameworks to track your global footprint.

This guide outlines the explicit reporting thresholds and rules for FBAR, FATCA, Form 8833, and the inverse requirements imposed by major European host nations.

1. US FinCEN Form 114 (FBAR)

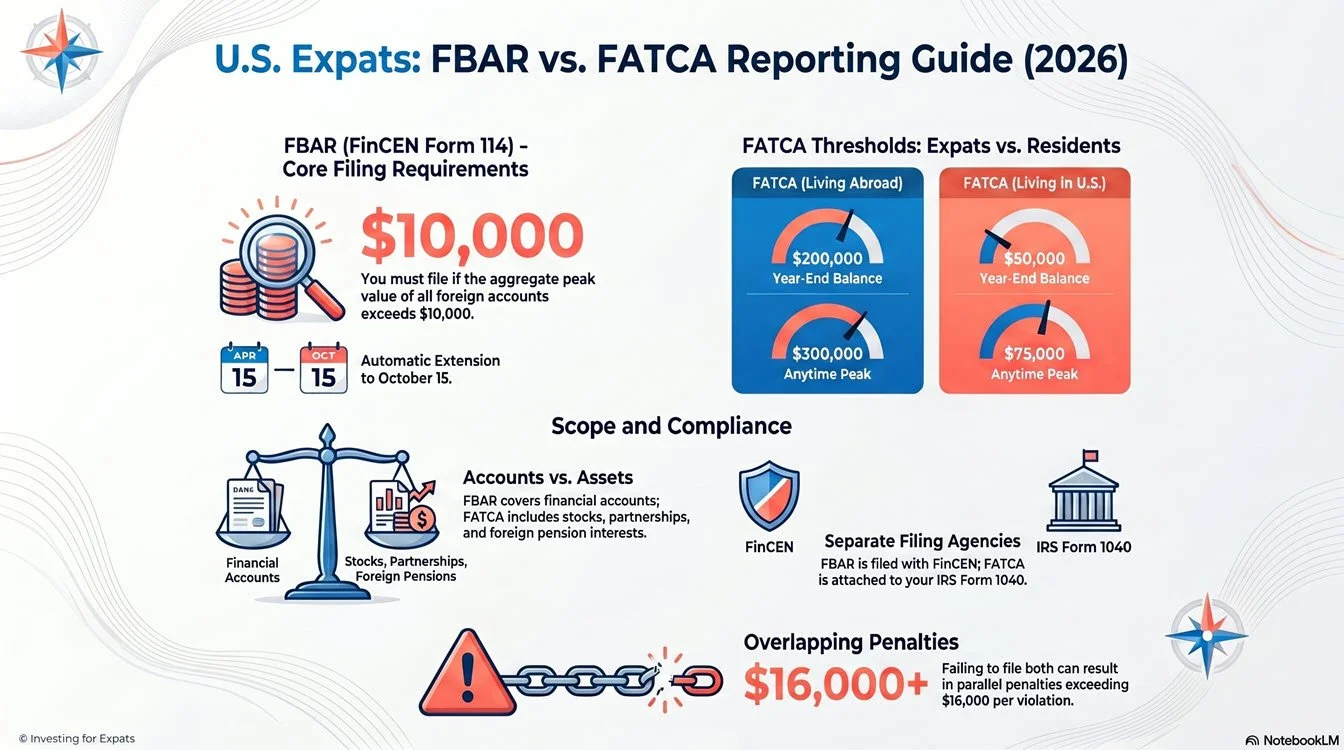

The Foreign Bank and Financial Accounts Report (FBAR) is a regulatory disclosure filed with the Financial Crimes Enforcement Network (FinCEN), completely separate from your IRS tax return.

The Trigger Threshold: You must file an FBAR if the aggregate maximum balance of all your foreign financial accounts exceeds $10,000 at any single point during the calendar year.

The Aggregate Trap: The threshold is not per account. If you hold three foreign retirement or bank accounts that briefly hit $4,000 each on the exact same day, your total is $12,000, and all three accounts must be reported.

What Counts: Local European workplace pensions, personal pensions (e.g., UK SIPPs, German Rürup-Rente), foreign brokerage accounts, and standard bank accounts. Signature authority over a corporate or employer account also pulls that account onto your personal FBAR if the threshold is met.

Filing & Deadlines: Filed electronically via the FinCEN BSA E-Filing System. It mirrors the standard tax deadline (April 15) but carries an automatic extension to October 15 with no paperwork required.

Penalties: Civil penalties for non-willful failures are capped at $16,536 per report (per year, not per account). Willful violations scale up to the greater of $165,353 or 50% of the account balance per violation.

2. IRS Form 8938 (FATCA)

Enacted under the Foreign Account Tax Compliance Act (FATCA), Form 8938 is attached directly to your federal income tax return (Form 1040). Because Congress recognized that expats naturally hold larger foreign balances for local living expenses, the thresholds for Americans living abroad are substantially higher than domestic filers.

To qualify for these higher expat thresholds, you must meet either the Bona Fide Residence test or the Physical Presence test (330 full days abroad in a 12-month period).

2026 FATCA Reporting Thresholds for Expats

What Counts: This goes beyond bank accounts. It includes foreign pensions, deferred compensation plans, foreign stock certificates held directly outside a brokerage, partnership interests, and cash-value life insurance policies issued by foreign companies.

Filing & Deadlines: Submitted as part of your Form 1040 package. Expats receive an automatic two-month extension to June 15, which can be extended to October 15 via Form 4868.

Penalties: An initial $10,000 failure-to-file penalty, with continuous non-compliance penalties scaling up to an additional $50,000. Furthermore, a 40% accuracy-related penalty can be slapped on any underpayment of tax linked to undisclosed foreign assets.

3. IRS Form 8833 (Treaty-Based Return Position Disclosure)

Form 8833 tells the IRS that you are using a bilateral international tax treaty to override or modify standard internal revenue codes.

When It Is Required: You must file Form 8833 if a treaty allows you to claim a Foreign Tax Credit that the tax code wouldn't normally allow, or if you are changing the statutory source of income to avoid US taxation. For example, if you are a dual-resident taxpayer claiming foreign residency under a treaty tie-breaker rule and your affected income items exceed $100,000, Form 8833 is mandatory.

When It Is Waived (The Pension Exception): Under Treasury Regulations section 301.6114-1(c), the IRS waives the Form 8833 filing requirement for individuals claiming treaty exemptions or reduced withholding on standard pension distributions, annuities, or Social Security payments.

The Penalty: If you take a reportable treaty position but fail to attach Form 8833, the statutory penalty is $1,000 per occurrence for individuals, even if the underlying treaty position you took is 100% legal.

4. European Host Country Reporting Requirements

Reporting is a two-way street. While you report your European accounts to the US, your European host country requires visibility into your US-based assets (like traditional IRAs, 401ks, and Roth accounts).

United Kingdom (HMRC)

Mechanics: The UK does not have a wealth tax or a direct equivalent to the FBAR for simply holding US assets.

The Trigger: Reporting triggers purely upon realization or distribution. Under Article 17 of the US-UK treaty, traditional 401(k) and IRA distributions must be reported on your Self Assessment tax return as foreign pension income.

Roth Treatment: Under the treaty, a US Roth IRA is recognized as a qualified pension wrapper. As long as the distribution is qualified under IRS rules, it does not need to be reported as taxable income to HMRC.

France (Code Général des Impôts)

Form 3916 / 3916-bis: France requires all residents to declare all bank, brokerage, and digital asset accounts held outside of France annually. Your US IRAs, 401(k)s, and standard bank accounts must be detailed on this form alongside your main income tax filing (Form 2042).

Wealth Tax (IFI): While standard US retirement accounts are generally excluded from France's Property Wealth Tax (Impôt sur la Fortune Immobilière), any US-sited direct real estate holdings or real estate investment trusts (REITs) must be monitored if your global real estate net worth exceeds €1.3 million.

Germany (Finanzamt)

Anlage AUS & Anlage KAP: Germany taxes its residents on global income. While you do not file a standalone "asset disclosure" form like the FBAR, you must report global income, dividends, capital gains, and pension distributions from US accounts on Anlage AUS (Foreign Income) and Anlage KAP (Investment Income).

The Foreign Pension Trap: If you hold US mutual funds inside a standard, non-retirement US brokerage account, they are subject to Germany's complex Investment Tax Act (Investmentsteuergesetz), which can trigger punitive annual phantom taxation (Vorabpauschale) on unrealized gains.

Italy (Agenzia delle Entrate)

Quadro RW: This is Italy's strict equivalent to a combined FBAR and FATCA asset disclosure form. Any Italian tax resident holding financial assets or real estate abroad must complete Quadro RW. This includes the maximum and year-end values of all US traditional IRAs, 401(k)s, and Roth accounts.

Wealth Taxes (IVIE / IVAFE): Financial assets reported on Quadro RW are typically subject to IVAFE (Foreign Financial Assets Tax), which sits at 0.2% of the asset value. However, qualified US treaty-protected retirement accounts (like a 401k or Traditional IRA) can sometimes be exempted from the direct wealth tax calculation, though they must still be reported. Foreign real estate is subject to IVIE at 1.06%.

-

IRS Form 8938: Filing requirements & who must report (2026) - Taxes for Expats

FBAR vs. Form 8938: Key differences & thresholds (2026) - Taxes for Expats

FBAR Filing 2026: Complete Guide to FinCEN Form 114 - GTA Accounting Group

FBAR Explained: Filing Requirements, Deadlines, and Penalties for U.S. Expats

Form 8938: What U.S. Expats Must Report Under FATCA Rules | Bright!Tax

FBAR penalties in 2026: Guide to late filing fees & relief - Taxes for Expats

FATCA threshold: Guide for Americans and US expats - Wise

FATCA Explained: Form 8938 Filing Requirements for Expats

What is the FATCA reporting threshold for married couples filing jointly and living abroad?

Treaty Based Return Reporting Disclosure - Form 8833

Form 8833 for Expats Explained: How to Claim Tax Treaty Benefits

Form 8833 treaty-based return position disclosure for expats - Taxes for Expats

Last Updated: May 28, 2026