European countries that tax Roth distributions of US residents.

European countries that tax Roth distributions of US residents

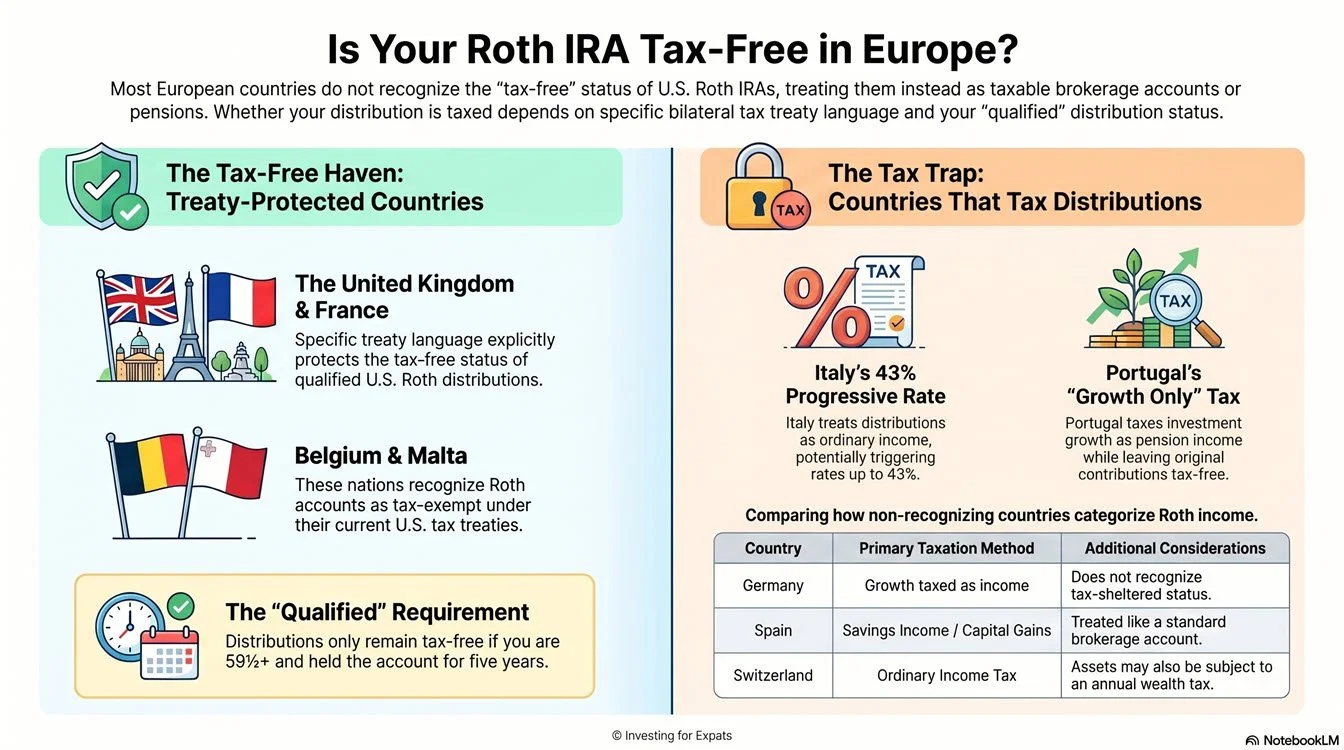

The vast majority of European countries tax distributions from U.S. Roth IRA accounts.

The default rule is that your country of residence has the right to tax your worldwide income, including pensions. Most countries do not recognize the unique "tax-free" status of a Roth account. They typically treat it as a standard investment account, meaning they will tax the growth (gains and earnings) of the account as income upon withdrawal.

Below is a list of European countries known to tax Roth IRA distributions, followed by the short list of known exceptions.

European Countries That Tax Roth IRA Distributions

This list includes countries where it is confirmed that Roth IRA distributions are subject to local taxes. The method of taxation may differ—some may tax only the gains, while others might tax the entire distribution.

Germany: Does not recognize the tax-free status of Roth accounts. The growth in the account is subject to German income tax.

Italy: Does not recognize the tax-free status. Roth distributions are typically treated as taxable income.

Spain: Does not recognize the Roth as a tax-sheltered vehicle. The account is treated like a standard brokerage account, and the profits/gains are subject to Spanish capital gains tax (the "savings income" tax) when withdrawn.

Portugal: Does not recognize the tax-free status. The capital growth (earnings) in the account is treated as pension income and is taxable in Portugal.

Switzerland: Does not recognize the Roth IRA as an equivalent to its own pension plans. It is treated as a taxable financial product, and the returns/gains are taxed as ordinary income. The assets may also be subject to the Swiss wealth tax.

The Baltic States (Estonia, Latvia, Lithuania): The tax treaties with these nations were established before Roth IRAs were common and lack the specific language needed to protect them. Therefore, they follow the default rule and are taxed by the country of residence.

General Rule: You should assume that any European country not on the "exceptions" list below will tax your Roth IRA distributions.

The Exceptions: Countries That Do NOT Tax Roth Distributions

A few European countries have modern tax treaties with the U.S. that contain specific provisions (often based on the 2006 U.S. Model Treaty) designed to recognize the tax-free status of accounts like Roth IRAs.

United Kingdom: Qualified Roth IRA distributions are tax-free in the UK. The US-UK tax treaty contains specific language that protects the tax-free nature of U.S. pensions, and this protection extends to Roth accounts.

France: Qualified Roth IRA distributions are tax-free. The US-France tax treaty is one of the most favorable for U.S. retirement accounts and explicitly recognizes their tax-free status.

Belgium: Qualified Roth IRA distributions are tax-free. The treaty with Belgium includes provisions that protect Roth accounts from taxation.

Malta: The technical explanation of the US-Malta tax treaty explicitly uses the Roth IRA as an example of an account that would be tax-exempt in Malta.

Important Considerations

"Qualified" is Key: This tax-free status only applies to qualified distributions (generally, you are over 59½ and have held the Roth account for at least 5 years). A non-qualified distribution will almost certainly be taxable everywhere.

This is Not Tax Advice: This information is based on analysis of tax treaties, which are complex legal documents. Their interpretation can change, and how they are applied in practice can be nuanced.

The "Saving Clause": Nearly all U.S. tax treaties contain a "Saving Clause," which allows the U.S. to tax its citizens as if the treaty didn't exist. This means that even if you live in France, your Roth distribution is still tax-free in the U.S. (as it always would be), and France also agrees not to tax it. The treaty's benefit is forcing the other country to honor the U.S. account's status.

Before making any financial decisions, it is essential to consult with a qualified cross-border tax professional who is an expert in both U.S. expat tax law and the specific tax laws of your country of residence.

Questions? Ask our research assistant about the European Taxation of US Roth IRA Distributions

Last updated: May 10, 2026