A short list of potentially confusing financial and tax terms with a focus on where the US and UK meanings differ:

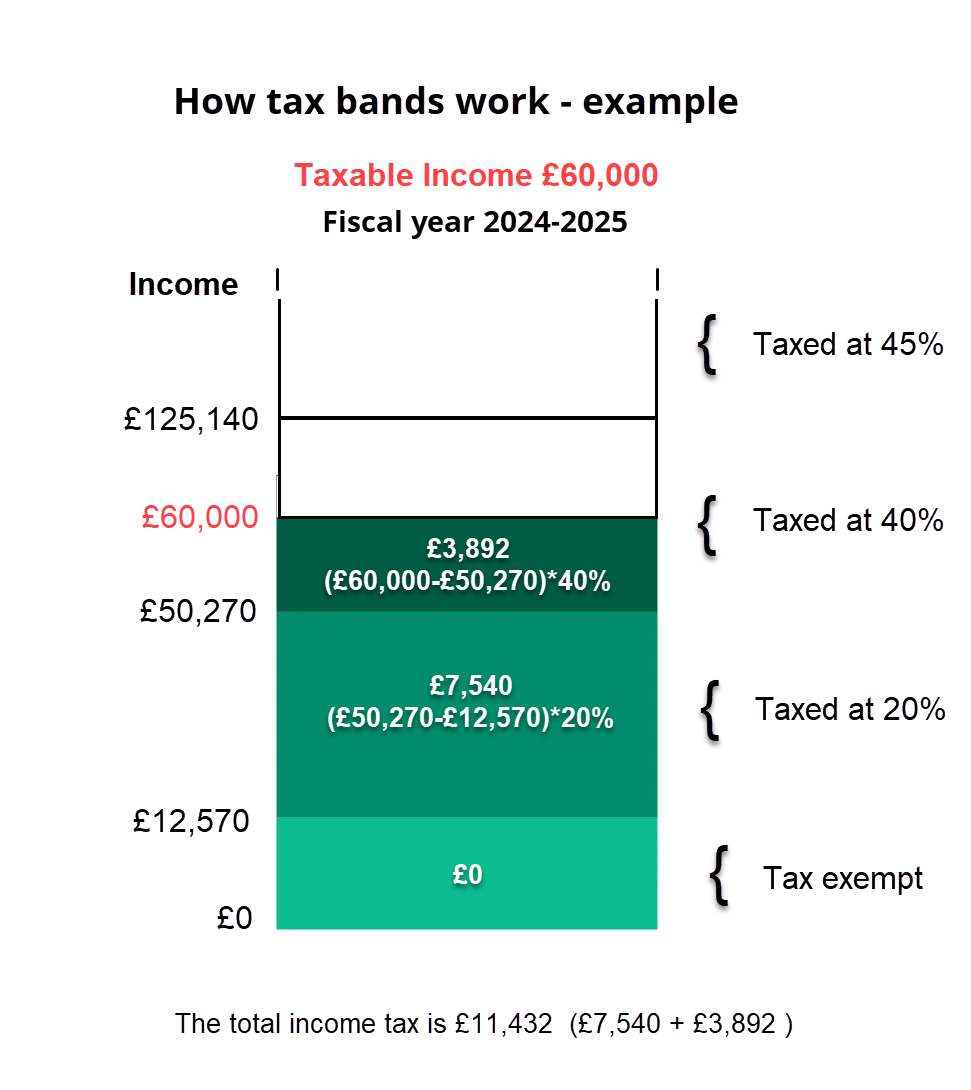

Tax Brackets vs. Tax Bands: Both systems have a progressive income tax structure where higher income is taxed at higher rates. However:

US: Uses "brackets" to define income ranges (e.g., 10% bracket, 22% bracket).

UK: Uses "bands" for income ranges (e.g., Basic rate band, Higher rate band).

US Treasuries vs. UK Gilts: US Treasuries, sometimes referred as T-bonds and UK Gilts (short for "gilt-edged securities") are both government bonds, meaning they are debt instruments issued by their respective governments to finance spending. However, there are some key differences.

Treasuries range in maturity from a few weeks to 30 years, Gilts range in maturity from a few months to 50 years .Treasuries are often considered a safe-haven asset due to the US government's strong credit rating while Gilts can offer higher yields but may be perceived as riskier due to the UK's smaller economy and potential political instability.

HMRC vs IRS: The HMRC administers the UK tax system and is responsible for various welfare programs. It is an agency similar to the IRS in the US. While both collect income tax, HMRC handles a broader range of taxes (like VAT), while the US relies on separate state-level sales taxes.

National Insurance (NI): This UK payroll tax has no precise equivalent in the US. While US Social Security and Medicare contributions share some similarities, NI is a separate system with specific eligibility rules and benefits.

PAYE (Pay As You Earn): In the UK, PAYE is a system where employers deduct income tax and National Insurance contributions (social security) directly from employees' wages before they are paid.

In the US, while employers also withhold federal income tax, state income tax (where applicable), and Social Security and Medicare taxes, the overall system is more complex due to variations in state and local taxes.

Stamp Duty Land Tax (SDLT): A tax on property transactions in the UK, unfamiliar to most Americans. This is an upfront cost in addition to the purchase price.

US Property Tax vs UK Council Tax: US Property Tax and UK Council Tax are both local taxes levied on property owners, but they have several key differences. In the US property taxes primarily fund public schools, local infrastructure, and other services provided by local governments. The UK council tax primarily funds local services such as waste collection, street lighting, libraries, and social care.

The US Property Tax rates vary significantly depending on the state, county, and city, and can change annually. The UK Council Tax rates vary depending on the local authority and the valuation band of the property. They are set annually.

Taxable Income: In the UK, taxable income includes earnings from employment, most pensions, rental income, and interest on savings above a certain threshold, while non-taxable income covers certain benefits, lottery winnings, and ISAs.

In the US, taxable income encompasses wages, salaries, tips, interest, dividends, and rental income, among others. Non-taxable income in the US includes certain gifts, inheritances, and specific types of insurance payouts. The specifics can vary widely based on legislation and individual circumstances in each country.

Expat vs Expatriate: In most everyday contexts, "expat" is a widely understood and accepted shortening of "expatriate," referring to anyone residing outside their country of citizenship.

However, it is essential for U.S. citizens to recognize the distinct legal definition of "expatriate" under U.S. tax law, which relates to the formal renunciation of citizenship or permanent resident status and carries significant tax implications. This legal definition is separate from the general use of "expat" to describe living abroad.

In the UK, the legal procedure for giving up British citizenship is known as renunciation, and a person who has renounced British citizenship can accurately be described as an expatriate.

Fiscal Year / Tax Year:

US: Tax year aligns with the calendar year (Jan 1st - Dec 31st)

UK: Tax year runs from April 6th to April 5th.

VAT (Value Added Tax): This consumption tax is included in the displayed goods and services prices. It is a tax similar to sales taxes in the US, but VAT is a national tax with less regional variation. The standard rate of VAT in the UK as of April 2025 is 20%. This rate applies to most goods and services.

Capital Gains Tax (CGT): Both countries tax gains on the sale of assets, but the rules and exemptions differ. The US distinguishes between short and long term gains, with short term gains taxed as regular income, while for the UK there is no such distinction. CGT rates and brackets also differ. The UK's annual CGT exemption can be a significant factor for US expats.

The US Estate Tax vs the UK the Inheritance Tax (IHT). This is a tax on the estate (the property, money, and possessions) of someone who has died. Key Differences between the two tax systems are:

• Scope: The U.S. has a citizenship-based tax system, whereas the U.K. emphasizes long-term residency beginning on April 6, 2025.

• Exemptions: The US has a significantly larger estate tax exemption than the UK's Nil rate band (or NRB), the amount up to which an estate has no inheritance tax to pay.

• Marital Transfers: US citizens can leave unlimited assets to their US-spouse tax-free, but this is not the case in the UK.

Gift Tax: The US gift tax is part of the federal tax system, designed to prevent tax-free wealth transfer during a person's lifetime. In the UK, there is no specific gift tax. However, gifts can be subject to Inheritance Tax if the giver dies within seven years of making the gift and their estate exceeds the nil-rate band.

Step-up in basis vs re-basing: Step-up in basis, also known as stepped-up basis, is a tax concept in the US that applies when you inherit an asset. It offers a tax benefit to heirs by resetting the cost basis of the inherited asset to its fair market value (FMV) on the date of the decedent's death.

In the UK, the equivalent concept to the US "step-up in basis" is known as "re-basing" for Capital Gains Tax (CGT) purposes. However, the principles and applications of this concept can differ significantly from the US system.