Investment options for a UK citizen residing in the US who is saving for retirement

Summary

This article outlines retirement investment options available to a UK citizen residing in the US, distinguishing between resident and nonresident alien status for tax purposes. For US resident aliens, it details employer-sponsored plans like 401(k)s and 403(b)s, individual retirement accounts (Traditional and Roth IRAs), and other options like SEP IRAs and Solo 401(k)s, also addressing income limits and tax treatment for each. The text further compares the lower costs of investing in the US versus the UK and highlights the impact of fees on portfolio growth. Finally, it discusses the impossibility of directly transferring UK pensions to US retirement accounts and presents various long-term and short-term savings options available in the US.

Residency:

If you are not a U.S. citizen, you are considered a nonresident of the United States for U.S. tax purposes unless you meet one of two tests. You are a resident of the United States for tax purposes if you meet either the green card test or the substantial presence test for the calendar year (January 1 – December 31). If you are not a U.S. citizen and don’t meet either of these tests you are considered a nonresident of the United States for U.S. tax purposes and these tax-favored plans are not available to you.

As a U.S. resident alien, you have several options for saving for retirement, similar to U.S. citizens:

Employer-Sponsored Plans:

401(k): If your employer offers a 401(k) plan, this is an excellent way to save for retirement. You can make pre-tax contributions, and your employer may offer matching contributions. If your employer offers matching contributions to a retirement plan, take full advantage of it.

403(b): Similar to a 401(k), but offered by non-profit organizations and some public schools.

Individual Retirement Accounts (IRAs):

Traditional IRA: Contributions may be tax-deductible, and your investment grows tax-deferred until retirement.

Roth IRA: Contributions are not tax-deductible, but qualified withdrawals in retirement are tax-free.

Other Options:

Simplified Employee Pension (SEP) IRA: If you're self-employed or own a small business, a SEP IRA allows you to contribute a higher percentage of your income than a traditional IRA.

Solo 401(k): Another option for self-employed individuals, offering higher contribution limits than IRAs.

Taxable Brokerage Accounts: You can also invest in stocks, bonds, mutual funds, and other assets through a taxable brokerage account. While these don't offer the same tax benefits as retirement accounts, they provide flexibility and liquidity when you need it.

Income Limits:

Traditional IRA: Your ability to deduct contributions to a traditional IRA is limited based on your Modified Adjusted Gross Income (MAGI) and tax filing status.

If you are covered by a workplace retirement plan (like your UK company pension), the deduction may be phased out or eliminated depending on your income level. Since your UK pension contributions reduce your U.S. taxable income, this could impact your eligibility for the deduction.

If you are not covered by another plan, there is no income limit for deductibility.

Roth IRA: Contributions to Roth IRAs are subject to income limits. If your MAGI exceeds certain thresholds, you may not be able to contribute the full amount or at all. Your UK pension contributions can affect your eligibility for Roth IRA contributions, as they can lower your MAGI.

Tax Treatment:

Traditional IRA:

Contributions: May be tax-deductible on your U.S. tax return, reducing your taxable income for the year.

Growth: Tax-deferred until withdrawal.

Withdrawals: Taxed as ordinary income in the U.S.

Roth IRA:

Contributions: Not tax-deductible.

Growth: Tax-free if certain conditions are met.

Withdrawals: Qualified withdrawals are tax-free.

401(k):

Contributions: Usually made pre-tax, lowering your taxable income.

Growth: Tax-deferred until withdrawal.

Withdrawals: Taxed as ordinary income in the U.S.

UK Company Pension:

Contributions: Often tax-deductible in the UK, reducing your UK taxable income and potentially your U.S. taxable income due to the Foreign Tax Credit or Foreign Earned Income Exclusion.

Growth: Tax-deferred in the UK until withdrawal.

Withdrawals: Subject to UK income tax. Depending on the U.S./UK tax treaty, you may also owe U.S. tax, but you can usually claim a foreign tax credit to avoid double taxation.

Tips:

Start Early: The sooner you start saving, the more time your investments have to grow.

Maximize Contributions: Contribute as much as you can afford to your retirement accounts each year.

The cost of investing in the U.S. compared to the U.K.

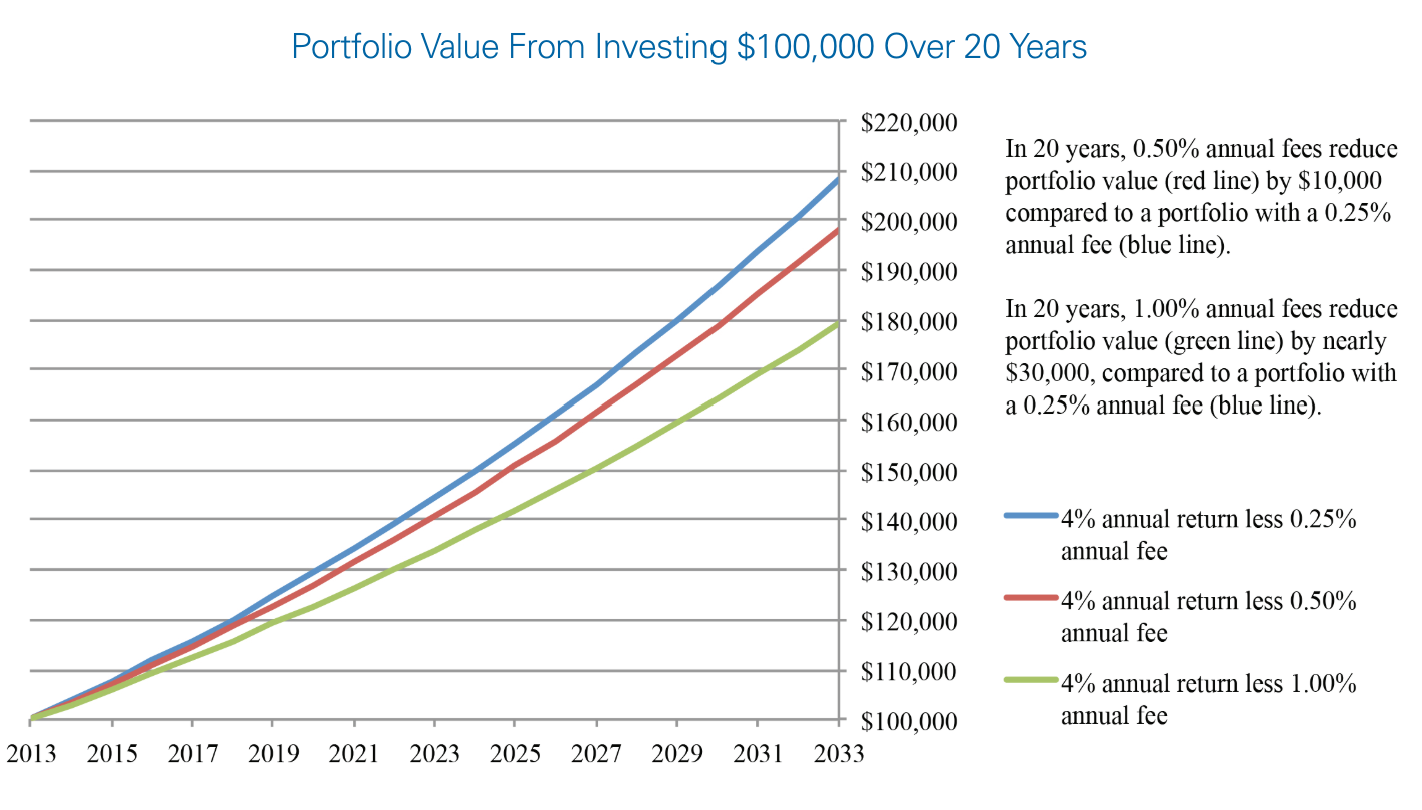

The cost of investing in the U.S. is generally lower compared to the U.K. In the U.S., fees are often nonexistent for many ETFs and stocks. In contrast, in the U.K., charges are calculated as a percentage of the investment amount, sometimes reaching 2% or more annually. While this percentage might seem modest, it can have a significant impact.

For instance, consider an investment of $100,000 with a 4% annual return. “In 20 years, 1% annual fees reduce your portfolio value by nearly $30,000 compared to a portfolio with 0.25% annual fee”. Over time, even small ongoing fees can significantly impact your investment portfolio’s return.

Important Considerations for a British Expat:

Taxation: The US-UK tax treaty generally aims to prevent double taxation but understanding how different investment income is taxed in both countries is key to investing success.

Foreign Exchange: Fluctuations between the US dollar (USD) and British pound sterling (GBP) can impact your returns, both positively and negatively.

Remember you might be subject to the US Social Security system if you work in the US for a certain period, which may provide you valuable benefits during retirement.

Can you transfer your UK pension to the US? Transferring your UK pension directly to a US retirement plan like a 401(k) or IRA is unfortunately not possible under current regulations. Here's why:

Tax Implications: The US and UK have different tax laws for retirement savings. Transferring directly could trigger tax penalties in the UK and potentially disqualify your funds from US tax advantages.

Recognition by US Authorities: The US Internal Revenue Service (IRS) doesn't currently recognize many UK pension schemes as qualified plans for rollovers.

While transferring directly isn't possible, there are still ways to manage your UK pension alongside a US retirement plan. Depending on your age and circumstances, you might be able to withdraw some or all of your pension as a lump sum. However, this could trigger tax penalties and limit your retirement income.

Long-term Savings Options

Long-term saving options are investment vehicles designed to help you grow your wealth over an extended period, typically 10 years or more. The best option for you depends on your risk tolerance, financial goals, and time horizon. Here are some popular choices:

Individual Stocks: Investing in individual companies can offer significant growth potential, but it also carries higher risk.

Exchange-Traded Funds (ETFs): These allow you to invest in a diversified portfolio of stocks, spreading the risk.

Individual Bonds: Loans you make to companies or governments, offering regular interest payments and the return of principal at maturity.

Rental Properties: Generate ongoing income and potential appreciation over time.

Real Estate Investment Trusts (REITs): Companies that own and operate income-producing real estate. You can invest in them through stocks.

Short-term Savings Options

While retirement savings are generally considered a long-term investment, there are short-term savings options you can use within your retirement accounts to provide stability and liquidity. Here are a few choices:

High-Yield Savings Accounts: These online accounts typically offer higher interest rates than traditional banks. Look for accounts insured by the FDIC (Federal Deposit Insurance Corporation).

Certificates of Deposit (CDs): CDs offer fixed interest rates over a specific term. Early withdrawal usually results in penalties.

Money Market Accounts: These are interest-bearing accounts with some check-writing and debit card access, making them a blend of savings and checking accounts.

Cash

Frequently Asked Questions for UK Citizens in the US Saving for Retirement

1. As a UK citizen living and working in the US, how is my residency status determined for US tax purposes related to retirement savings? Your residency status for US tax purposes is primarily determined by the "green card test" (holding lawful permanent resident status) or the "substantial presence test" (being physically present in the US for a certain number of days over a three-year period). If you do not meet either of these tests, you are considered a nonresident alien, and you are generally ineligible for US tax-advantaged retirement plans like 401(k)s and IRAs.

2. What retirement savings options are available to me in the US if I am considered a resident alien for tax purposes? As a US resident alien, you have several options similar to US citizens:

Employer-Sponsored Plans: 401(k) plans (with potential employer matching) and 403(b) plans (offered by non-profits).

Individual Retirement Accounts (IRAs): Traditional IRAs (contributions may be tax-deductible, growth tax-deferred) and Roth IRAs (contributions are not tax-deductible, qualified withdrawals are tax-free).

Self-Employed Options: SEP IRAs and Solo 401(k)s, which often allow for higher contribution limits.

Taxable Brokerage Accounts: Offer flexibility but lack the tax advantages of retirement accounts.

3. How do my contributions to a UK company pension affect my eligibility for and the tax treatment of US retirement accounts like Traditional and Roth IRAs? Contributions to your UK company pension can impact your eligibility for US IRAs. For Traditional IRAs, if you are covered by a workplace retirement plan (including your UK pension), the deductibility of your IRA contributions may be limited or eliminated based on your Modified Adjusted Gross Income (MAGI). Since UK pension contributions can reduce your US taxable income, they can lower your MAGI, potentially affecting your deduction eligibility. For Roth IRAs, there are income limits for contributions. Your UK pension contributions, by potentially lowering your MAGI, can affect whether you are eligible to contribute and the maximum amount you can contribute.

4. What are the key differences in tax treatment between Traditional IRAs, Roth IRAs, and 401(k)s in the US, and how might my UK pension fit into this tax landscape?

Traditional IRA: Contributions may be tax-deductible in the US, growth is tax-deferred, and withdrawals in retirement are taxed as ordinary income in the US.

Roth IRA: Contributions are not tax-deductible, growth is tax-free, and qualified withdrawals in retirement are also tax-free.

401(k): Contributions are usually pre-tax (lowering your US taxable income), growth is tax-deferred, and withdrawals in retirement are taxed as ordinary income in the US.

UK Company Pension: Contributions are often tax-deductible in the UK (potentially affecting your US taxable income through foreign tax credits or the Foreign Earned Income Exclusion), growth is tax-deferred in the UK, and withdrawals are subject to UK income tax. Under the US-UK tax treaty, you may also owe US tax on withdrawals, but you can typically claim a foreign tax credit to avoid double taxation.

5. Is it possible to transfer my existing UK pension savings directly into a US retirement account like a 401(k) or IRA? Directly transferring your UK pension to a US retirement plan (like a 401(k) or IRA) is generally not possible under current regulations. This is primarily due to differences in tax laws between the US and the UK, which could lead to tax penalties in the UK and disqualify the funds from US tax advantages. The US IRS does not typically recognize UK pension schemes as qualified plans for rollovers.

6. What should a UK expat in the US consider regarding investment costs and fees when choosing retirement savings options compared to the UK? Investment costs in the US are often lower than in the UK. In the US, many ETFs and stocks have no transaction fees. In contrast, the UK often charges fees as a percentage of the investment amount, sometimes reaching 2% or more annually. Even seemingly small percentage-based fees can significantly reduce your long-term investment returns. Therefore, UK expats in the US should pay close attention to the fee structures of US investment options and consider the potential long-term impact of these costs.

7. Beyond formal retirement accounts, what other long-term savings and investment options are available to a UK citizen residing in the US? Besides employer-sponsored plans and IRAs, UK citizens in the US can consider:

Taxable Brokerage Accounts: For investing in stocks, bonds, ETFs, and mutual funds without the tax advantages of retirement accounts but with greater flexibility.

Individual Stocks: Direct investment in companies, offering potential for high growth but also higher risk.

Exchange-Traded Funds (ETFs): Diversified investments in baskets of stocks, bonds, or other assets.

Individual Bonds: Lending to companies or governments for regular interest payments.

Rental Properties: Potential for income generation and appreciation.

Real Estate Investment Trusts (REITs): Investing in real estate through publicly traded companies.

8. What are some important financial considerations for a UK expat saving for retirement in the US, particularly regarding taxation and currency fluctuations? Key considerations include:

Taxation: Understanding the US-UK tax treaty to avoid double taxation on investment income and retirement withdrawals. It's crucial to be aware of how different types of income are taxed in both countries.

Foreign Exchange: Recognizing that fluctuations between the US dollar (USD) and British pound sterling (GBP) can impact the value of your investments and retirement income, especially if you plan to eventually return to the UK.

US Social Security: Understanding your potential eligibility for US Social Security benefits if you work in the US for a sufficient period.

Resources

IRS Website (Retirement Plans): https://www.irs.gov/retirement-plans

Investor.gov: https://www.investor.gov/

Moving to the US?

Our book "Investment Portfolio for US-UK Expats - The Secrets to Successful Cross-Border Investing" explains the critical steps you should take to avoid costly tax and investment mistakes. The book explores the essential criteria for building a low-risk, tax-efficient, and cost-effective investment portfolio tailored to individuals subject to U.S. and U.K. taxation, culminating in a practical example of such a portfolio.

Last Updated: 3/16/2025