Buying a Private Residence in the U.K. - The surprises

Summary

This article outlines key differences and considerations for a U.S. buyer purchasing property in the U.K. It highlights that the U.K. home-buying timeline is less predictable than in the U.S., and fixed-rate mortgages typically have shorter terms. Prospective buyers also need to understand the concepts of freehold and leasehold ownership.

The Stamp Duty Land Tax (SDLT) is a significant cost, which can be substantial, especially for existing homeowners and non-U.K. residents.

Furthermore, the text addresses the U.K.'s Council Tax and considerations for transferring funds, including potential U.S. tax implications and reporting requirements.

Finally, it touches on U.S. tax consequences when selling a U.K. property, including capital gains tax and the impact of exchange rate fluctuations.

Timeline

If you have ever purchased a home in the U.S., you know that the process usually does not take more than 45-60 days to complete, from the moment you identify the property of your dreams to the moment when you get the keys. This time includes the duration necessary to apply for and secure a bank loan.

However, setting similar expectations for acquiring a private residence in the U.K. might lead to surprises. The timeline in the U.K. is notably less predictable, largely due to the need to coordinate among various parties involved in the transaction.

Mortgage Length

It might also be necessary to set aside the expectation of securing a 15- or 30-year fixed-rate mortgage, which is a common feature in the U.S. housing market. In the U.K., mortgage interest rates typically remain fixed for only a short period (2 to 5 years), a practice that safeguards lenders against rising interest rates.

Freehold and Leasehold

For a U.S. buyer, it may be surprising to learn that when purchasing a home in the UK, attention must also be paid to whether the property is a freehold or a leasehold. In the United Kingdom, property ownership is primarily categorized into two main types: freehold and leasehold.

Owning a freehold means you own the property and the land it stands on outright, with no time limit on the period of ownership. Leasehold ownership means you have the right to use the property for a set period as defined by a lease agreement, after which ownership reverts back to the freeholder. Lease periods for properties can be long, frequently beginning at 99 years or even extending beyond. However, it's essential to ascertain the remaining duration of the lease, as this can significantly impact the property's value and your ability to alter or sell the property in the future.

The Stamp Duty Land Tax (SDLT)

Perhaps the most significant revelation for prospective U.S. purchasers is the Stamp Duty Land Tax (SDLT), levied on the acquisition of property or land above a certain value in England and Northern Ireland, with Scotland and Wales having similar but distinct charges.

For residential properties, the SDLT rate is structured in bands that increase progressively with the property price.

The SDLT is an upfront cost in addition to the purchase price. If you already own a home anywhere in the world, you'll usually have to pay 5% on top of the already steep SDLT rates. You'll also pay a 2% surcharge if you're buying a residential property in England or Northern Ireland and are NOT a UK resident.

There is an exemption from SDLT for first-time buyers on purchases up to £425,000.

You can find more info and a SDLT calculator at here.

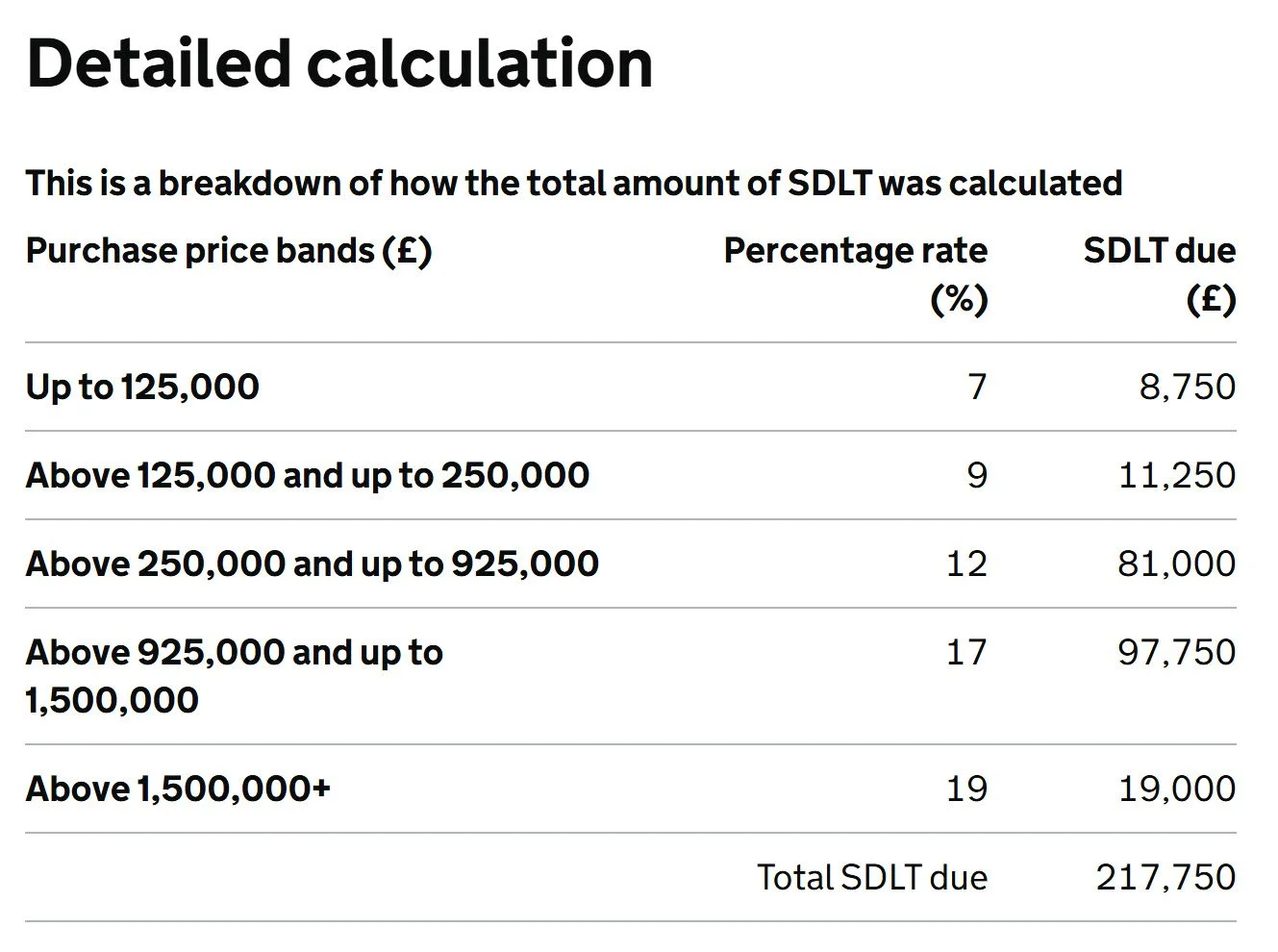

Example: you purchase a home in London for £1,600,000 and you already own a home in San Francisco and are not a UK resident, your SDLT would amount to £217,750.

Source: HMRC

Under these circumstances, opting to rent out your U.S. property might not be the most advantageous route. Additionally, it could be more beneficial to lease a property in the U.K. instead of buying one right away. Renting in the U.K. provides an opportunity to build your credit history there and gives you some breathing space to contemplate selling your U.S. home before committing to a purchase in England.

The Council Tax

The Council Tax (similar to the US property tax) is a yearly charge levied by your local council to fund its various services, including police and fire departments, waste collection, park upkeep, and library services. The fee you're required to pay is determined by your home's valuation band and its location. For more information, visit the MoneyHelper website.

Transferring the money to the U.K. to finance the purchase

If you need to transfer money to pay for the property, you may not be taxed if this happens during your first four years of residency in the U.K.

Starting April 6, 2025, new rules introduce a Foreign Income and Gains (FIG) regime that allows new residents who have lived outside the UK for at least 10 years to avoid UK taxes on foreign income and gains for their first four years, with certain conditions, and explicitly claiming relief based on the FIG regime on your self-assessment tax return for the year of transfer.

However, claiming relief will lead to a loss of your income tax allowance and capital gains exemption for the year. Therefore, a careful calculation is needed to determine what is more tax-efficient for you.

After these four years, you are taxed on your foreign Income and gains regardless of whether you remit the money to the UK.

If your parents can help you finance the purchase, such contributions would be considered a gift, and if your parents are not U.K. residents, there would not be U.K. tax consequences. However, such financial gifts might trigger U.S. gift tax considerations and reporting requirements for your parents if they exceed the annual exclusion limit. Nevertheless, actual taxes may not be due until the total gifts surpass the significant lifetime exemption amount.

When transferring money, keep in mind that if your total foreign (i.e., non-U.S.) financial accounts exceed $10,000 at any time during the year, you need to file a Report of Foreign Bank and Financial Accounts (FBAR) with the U.S. You may already meet this obligation before any transfer if you have been earning money in the U.K.

Additionally, for larger balances, you may need to submit Form 8938 alongside your U.S. tax return. The reporting thresholds for taxpayers living abroad are as follows:

“You are married filing a joint income tax return and the total value of your specified foreign financial assets is more than $400,000 on the last day of the tax year or more than $600,000 at any time during the year. These thresholds apply even if only one spouse resides abroad. Married individuals who file a joint income tax return for the tax year will file a single Form 8938 that reports all of the specified foreign financial assets in which either spouse has an interest.

You are not a married person filing a joint income tax return and the total value of your specified foreign financial assets is more than $200,000 on the last day of the tax year or more than $300,000 at any time during the year.”

While this obligation doesn't raise your taxable income, it does mean extra paperwork for you or your accountant. To sidestep the filing requirement, consider transferring the funds directly to the solicitor managing your property purchase, which can simplify the process.

U.S. Tax consideration when selling your U.K. home

For the U.K. tax system, normally “if you sell (or otherwise dispose of – for example, if you give away) your only or main home, you do not have to pay capital gains tax (CGT) on any profit if it has been your only or main home throughout the entire period of ownership. This is called main residence relief (or private residence relief).” If this is not your only home you could be subject to a 24% CGT.

Selling your home in the U.K. could potentially increase your U.S. Capital Gains Tax (CGT) obligations, ranging from 15% to 20% of the profit made on the sale. If the property in question was your primary residence, you're eligible to exempt up to $250,000 of the gain from your taxable income (or up to $500,000 for married couples filing jointly), thanks to the Section 121 exclusion[iv], assuming you pass the ownership and usage criteria tests.

Sounds straightforward? However, the situation gets more complex if there's a financial gain or loss due to changes in the exchange rate between the British Pound (GBP) and the U.S. Dollar (USD) from when you bought to when you sold the property. This fluctuation can alter the calculated capital gain or loss and, consequently, affect your tax bill.

Moreover, the proceeds from the sale could potentially increase your Modified Adjusted Gross Income (MAGI) beyond the threshold of $200,000 for singles or $250,000 for those married and filing jointly, subjecting you to an additional 3.8% tax on the gain through the Net Investment Income Tax (NIIT).

For detailed information regarding housing in London, United Kingdom:

download the “Navigating the London Property Market: A Guide for US Citizens” (Spring 2025, 40 pages, PDF format)

For detailed information regarding housing in Edinburgh. Scotland:

download the “Navigating the Edinburgh Property Market: A Comprehensive Guide for US Citizens” (Spring 2025, 41 pages, PDF format)

Frequently Asked Questions: Buying Property in the U.K. for U.S. Buyers

Q1. How does the timeline for buying a house in the U.K. compare to the U.S.? The process of buying a private residence in the U.K. generally takes significantly longer and is less predictable than in the U.S., where it typically completes within 45-60 days. The extended timeline in the U.K. is primarily due to the need for coordination among various parties involved in the transaction.

Q2. What are the key differences in mortgage options between the U.K. and the U.S.? Unlike the prevalence of long-term (15 or 30-year) fixed-rate mortgages in the U.S., U.K. mortgages typically have fixed interest rates for much shorter periods, usually ranging from 2 to 5 years. This practice provides greater protection for lenders against rising interest rates.

Q3. What is the significance of "freehold" and "leasehold" when buying property in the U.K.? In the U.K., property ownership is categorized as either freehold or leasehold. Freehold means you own the property and the land it stands on indefinitely. Leasehold means you have the right to occupy the property for a specified period defined by a lease agreement, after which ownership reverts to the freeholder. The remaining length of a leasehold can significantly impact a property's value and future saleability.

Q4. What is Stamp Duty Land Tax (SDLT), and how does it affect U.S. buyers? Stamp Duty Land Tax (SDLT) is a tax levied on property purchases above a certain value in England and Northern Ireland. It is a significant upfront cost in addition to the property price. For U.S. buyers who already own property anywhere in the world, an additional 5% surcharge typically applies on top of the standard SDLT rates. Non-U.K. residents buying residential property in England or Northern Ireland also pay a 2% surcharge. First-time buyers may be exempt on purchases up to £425,000.

Q5. What is Council Tax, and how does it compare to property taxes in the U.S.? Council Tax in the U.K. is an annual charge levied by local councils to fund local services, similar to property taxes in the U.S. The amount payable is determined by the property's valuation band and its location.

Q6. What are the U.K. tax implications when transferring funds from the U.S. to purchase a property? New residents in the U.K. who have lived outside the UK for at least 10 years may be able to avoid U.K. taxes on foreign income and gains transferred to the U.K. within their first four years under the Foreign Income and Gains (FIG) regime, effective from April 6, 2025, provided they explicitly claim relief. However, claiming this relief will result in the loss of their income tax allowance and capital gains exemption for that year, requiring a careful tax efficiency calculation. After the initial four years, foreign income and gains are taxable in the U.K. regardless of whether the money is brought into the country. Gifts from non-U.K. resident parents to help with a property purchase are generally not subject to U.K. tax.

Q7. What U.S. reporting requirements exist when transferring money from the U.S. to the U.K. for a property purchase? U.S. residents must file a Report of Foreign Bank and Financial Accounts (FBAR) if their total foreign financial account balances exceed $10,000 at any point during the year. For larger balances, Form 8938 may also need to be submitted with the U.S. tax return, with higher reporting thresholds for taxpayers living abroad. To potentially avoid these filing requirements, consider transferring funds directly to the solicitor managing the property purchase.

Q8. How might selling a U.K. property impact U.S. capital gains tax? While the U.K. offers "main residence relief" from Capital Gains Tax (CGT) if the sold property was your only or main home, selling a U.K. home can have U.S. CGT implications, potentially ranging from 15% to 20% of the profit. U.S. taxpayers may be eligible for the Section 121 exclusion, exempting up to $250,000 (single) or $500,000 (married filing jointly) of the gain if the property was their primary residence and they meet ownership and usage criteria. Fluctuations in the GBP/USD exchange rate between the purchase and sale dates can further complicate the calculation of capital gains or losses and affect the U.S. tax bill. Additionally, the sale proceeds might push your Modified Adjusted Gross Income (MAGI) above certain thresholds, potentially subjecting the gain to the 3.8% Net Investment Income Tax (NIIT).

Q9. Will leaseholds be eliminated in the UK?

While leasehold is not being entirely abolished in the UK, significant reforms are underway. The Leasehold and Freehold Reform Act will prohibit the sale of new leasehold houses in England and Wales, except in specific, exceptional cases. Furthermore, the government intends to eliminate leaseholds for all new flats through the proposed Leasehold and Commonhold Bill.

Sources:

Council Tax: what it is, what it costs and how to save money https://www.moneyhelper.org.uk/en/homes/buying-a-home/how-to-save-money-on-your-council-tax-bill

Summary of FATCA Reporting for U.S. Taxpayers https://www.irs.gov/businesses/corporations/summary-of-fatca-reporting-for-us-taxpayers

Selling your home https://www.litrg.org.uk/savings-property/capital-gains-tax/selling-your-home

Section 121 - Exclusion of gain from the sale of principal residence https://www.irs.gov/pub/irs-drop/rr-14-02.pdf

Leasehold and Commonhold Bill https://hoa.org.uk/advice/guides-for-homeowners/for-owners/leasehold-reform/

Last Updated: 5/30/2025